“Bubble-Like Stock Valuations Miss $3.4 Trillion in Hidden Assets” – or Why Intangibles Matter

June 08, 2018This week, in Bubble-Like Stock Valuations Miss $3.4 Trillion in Hidden Assets, Bloomberg detailed how traditional accounting can make a company’s fundamentals “look a lot worse than they are.” In the article, New York University’s Professor Baruch Lev weighs in. “You get numbers which are highly inflated for some companies and are understated for other companies.”

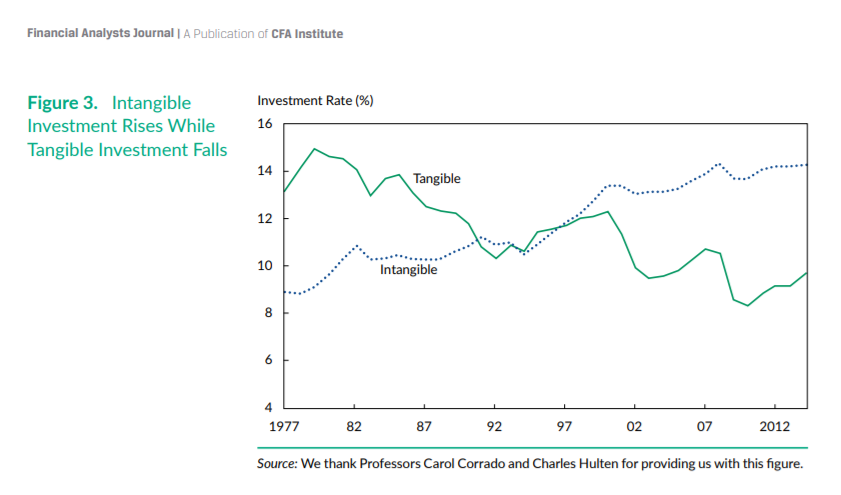

As companies’ intangible investments are on the rise, “spending on research and sales as a percentage of revenue rose to 14 percent in 2017 for S&P 500 stocks, compared with 7 percent a decade ago,” data compiled by Bloomberg show. Bloomberg’s findings are real, and in fact join a long history of research documenting the rise in intangible investment spending. Lev captured the trend in a chart in his 2017 article, Time to Change Your Investment Model.

The problem is, as Bloomberg accurately reports, under an accounting rule implemented in 1974, intangibles are expensed rather than capitalized, and “Not recognizing intangible assets can push down both profits and book value in businesses that depend on research and marketing, which are increasingly important in the global knowledge economy.”

As a result, this discrepancy has prevailed for decades. In the 1990s Lev conducted a series of studies analyzing 20 years of financial data and discovered an association between a firm’s level of knowledge capital and subsequent stock performance. Further research advanced the findings and in 2005, Lev proved the existence of a market efficiency — attributable to missing information about corporate knowledge investments – that leads highly innovative companies to deliver persistent abnormal returns.

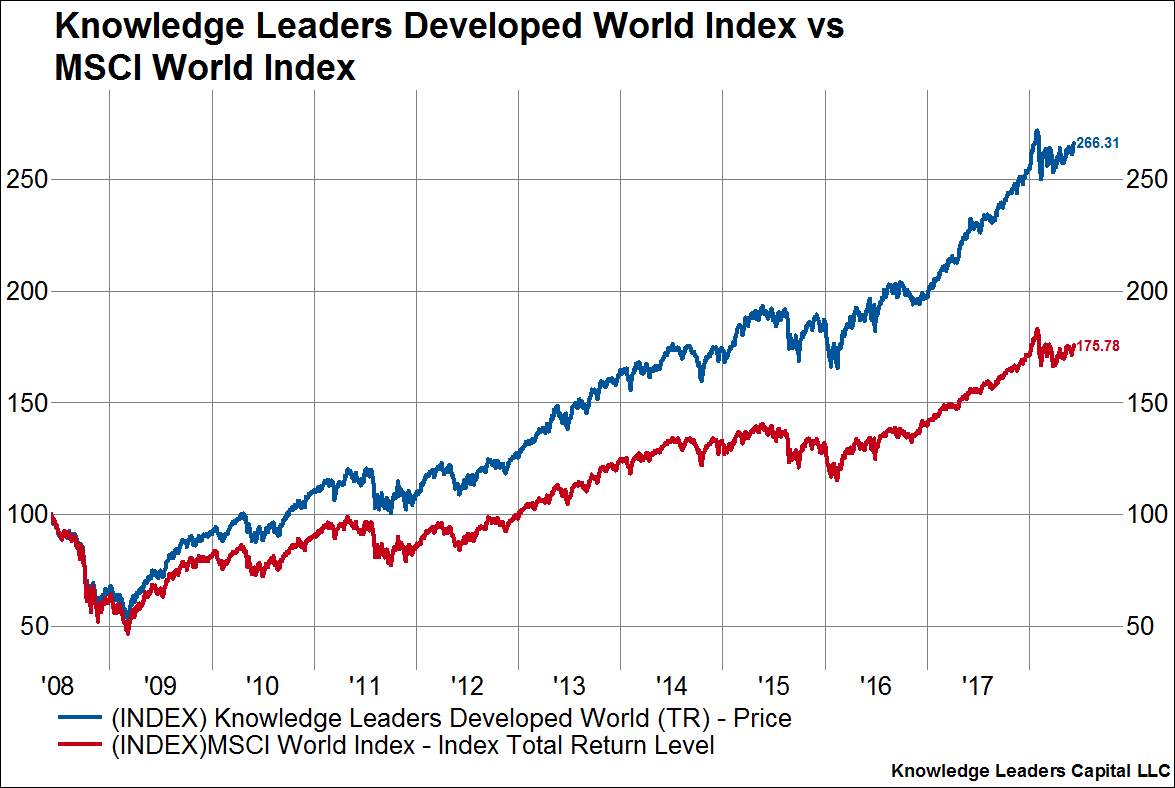

We call this market anomaly the Knowledge Effect, and building on Lev’s research, created the first real-time experiment that tests Lev’s findings. Through our proprietary model that adjusts a company’s financial statements to capitalize rather than expense intangible investments (including R&D, branding, IT, HR and organizational capital), we correct for this discrepancy that skews valuations for companies like Autodesk, as Bloomberg reports, “a company whose fundamentals are made to look a lot worse than they are by old, and increasingly useless, accounting rules.”

Once the data is adjusted for all 2,000 companies in our developed world universe, for example, we have a complete set of intangible-adjusted data. This is when trends emerge that separate the Knowledge Leaders from the Followers. Companies that meet certain thresholds in our model — such as % of sales spent on knowledge investments, for example — emerge as Knowledge Leaders and are included in the index.

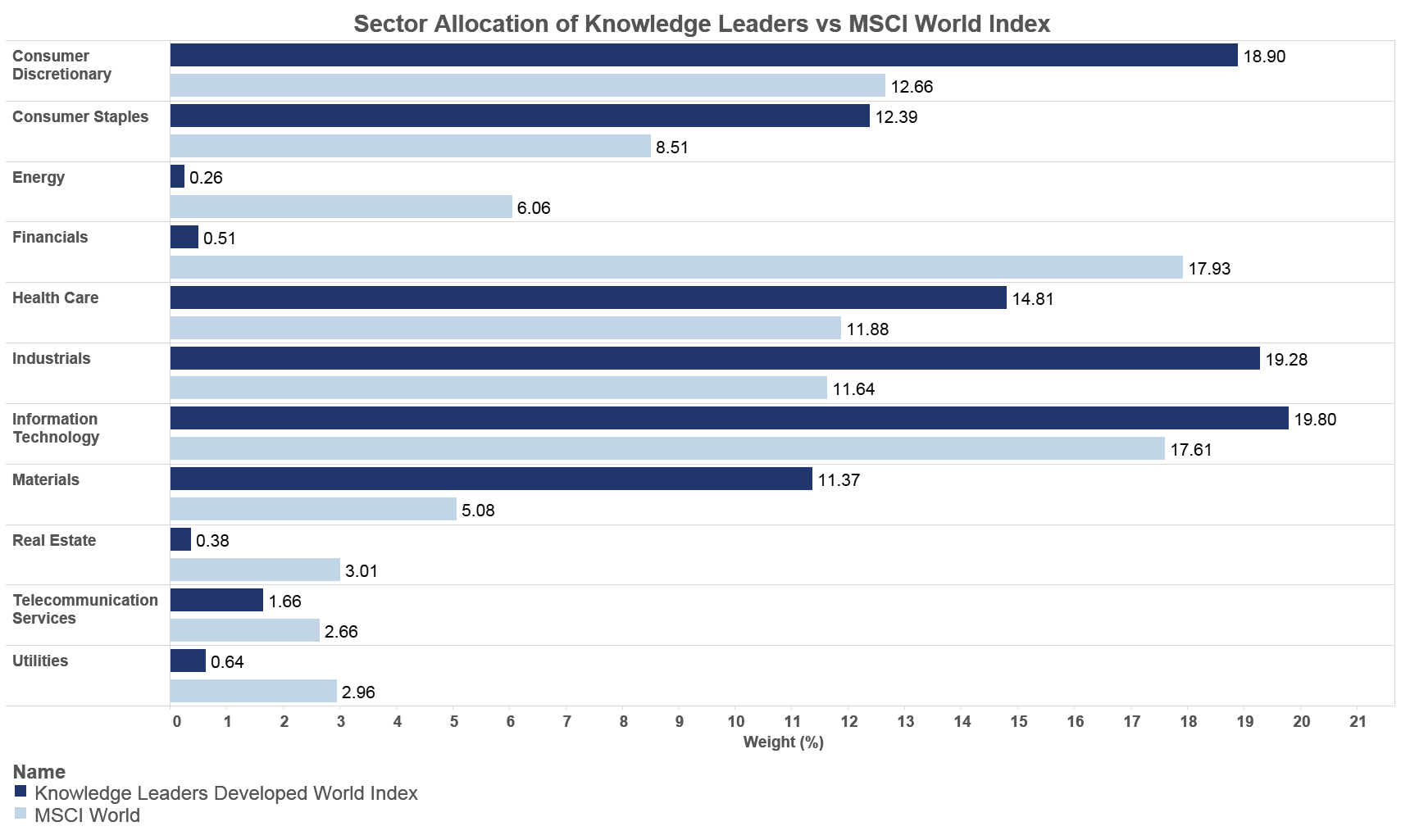

This distortion of company financial data due to non-capitalization of a company’s intangible assets is not just happening in technology firms like Autodesk. It’s a broad phenomenon. Through our model, we can identify Knowledge Leaders across the sectors, though some sectors spend more on intangible capital than others. You can see this breadth in recent “spotlight” articles, where we highlight different companies’ applications of intangibles. Find them here: Rio Tinto, Chevron, Shionogi, iRobot, Diageo and in the chart below.

There exist regional trends in investment in intangibles too. Some regions consistently spend more than others as we see in the chart below of Knowledge Leader representation in the geographies.

After adjusting for intangibles, we get a more accurate view of what – and whether – a company is investing in its future. This offers important clues to the firm’s overall value. In the Bloomberg article, Lev pointed to Kite Pharma Inc., “which had posted a loss every quarter since its public debut when Gilead Sciences Inc. bought it for $12 billion last year. What was Gilead after? Kite’s cancer therapies,” – in other words, the firm’s intangible capital, which remains hidden in traditional financial reporting.

“Investors are becoming much smarter — some, at least — and they are desperately looking for some information in those intangibles,” Lev told Bloomberg. “You capitalize, you amortize, and you have an income statement that says something, unlike today.”

As of 3/31/18, Autodesk, Gilead Sciences, Rio Tinto and Chevron Corp. were held in the Knowledge Leaders Strategy. An investor cannot invest directly in an index.