USD Hedging Getting More Expensive: LIBOR-OIS Spread Heading Higher

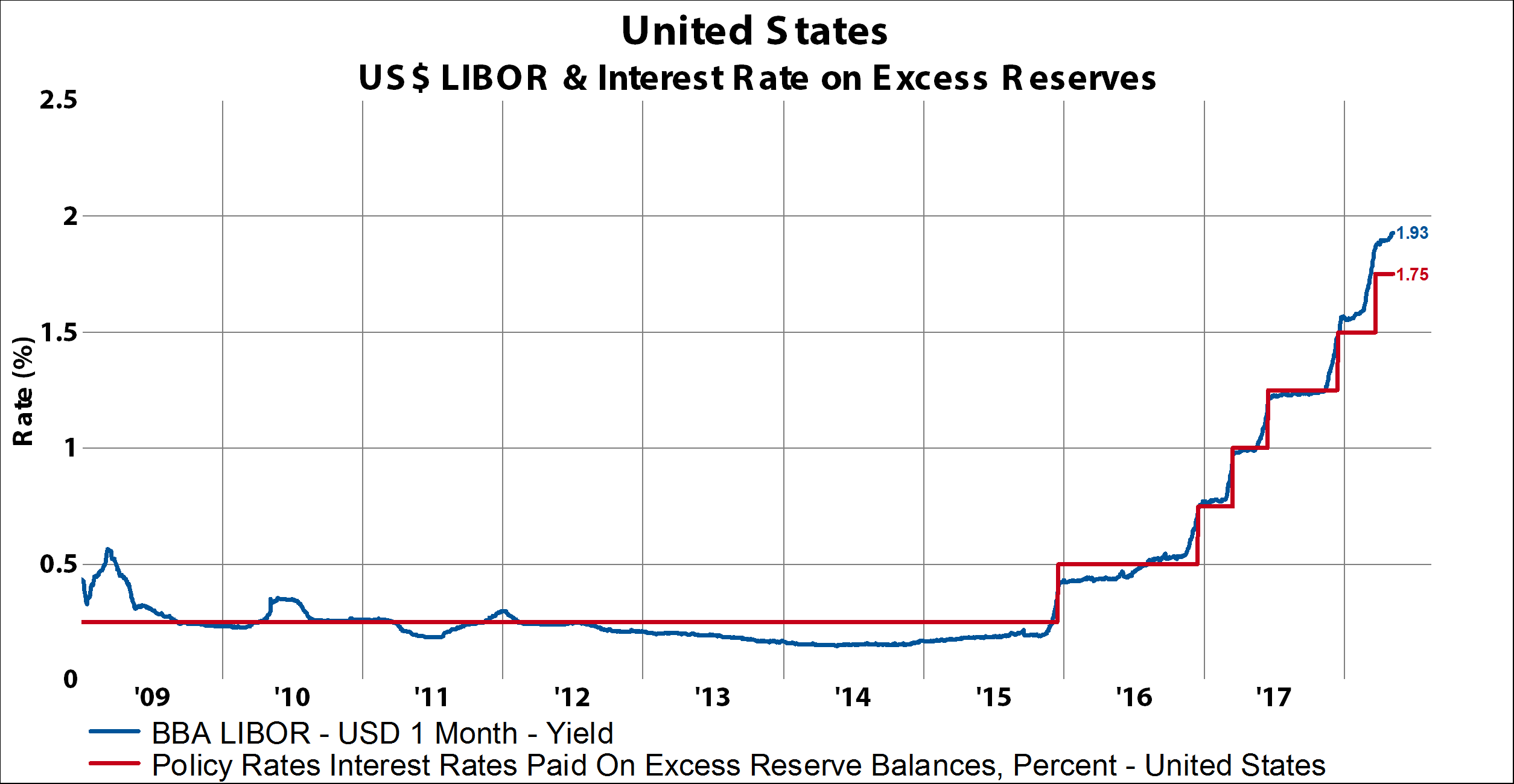

May 09, 2018There are two basic drivers of the London Interback Offered Rate (LIBOR): 1) policy rates and 2) a variable premium. Starting with the policy rates component, in the chart below I compare the interest rate on excess reserves (IOR) and USD LIBOR. Because the IOR rate is purely policy directed, I am using the interest on excess reserves as a surrogate to the overnight index swap (OIS) rate. Since there are about six more 25bps rate hikes expected by the end of 2019, USD LIBOR should track rates higher.

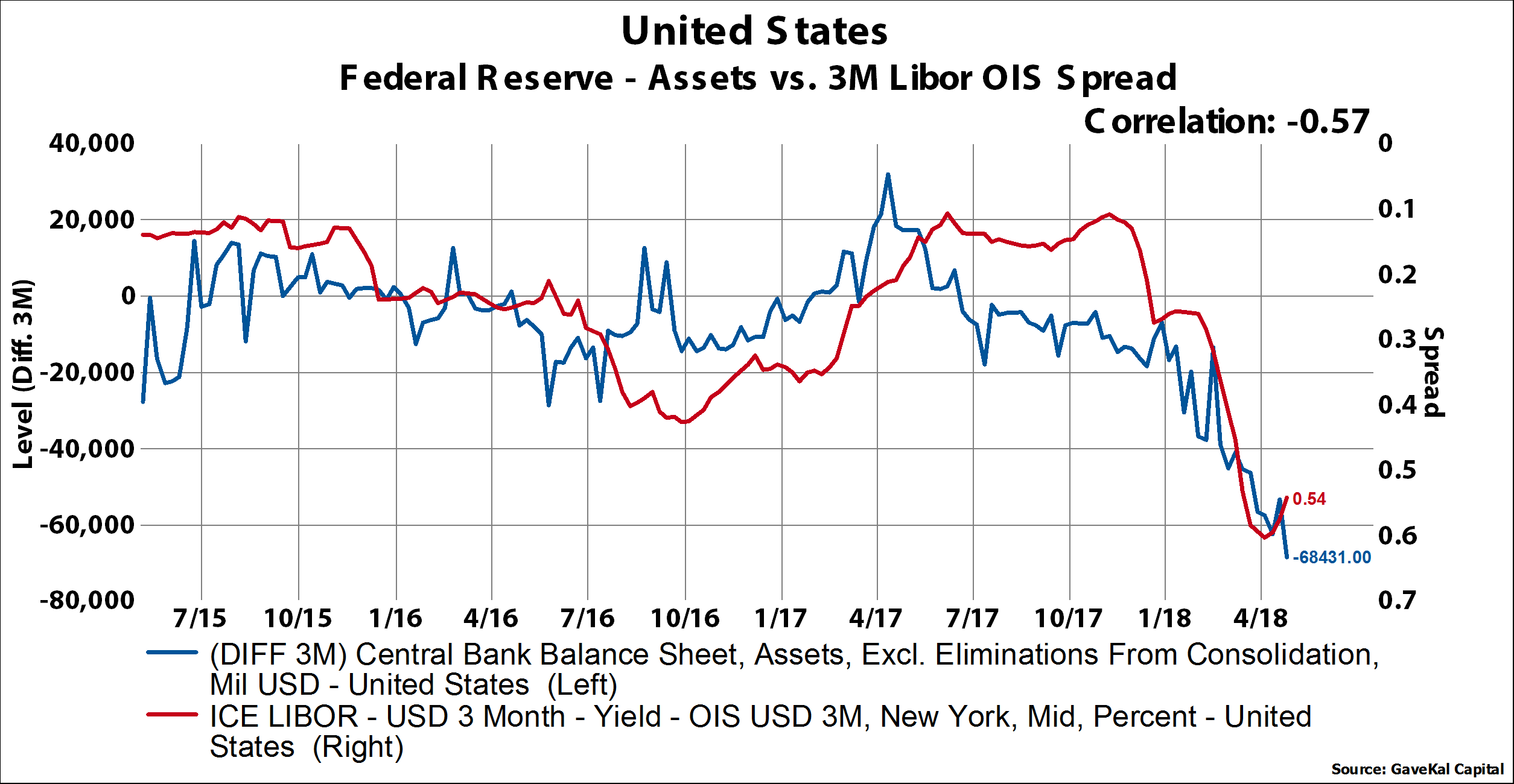

The second component of the LIBOR-OIS swap is a variable premium. Our work suggests the biggest driver of the variable premium is monetary driven also. So-called “quantitative tightening” is the term that has been adopted to describe the process of balance sheet roll-off at the Federal Reserve. In the chart below, I compare the 3-month change in the Federal Reserve’s balance sheet to the LIBOR-OIS spread. In the last few months, as the Fed has held to its accelerated pace of run-off, the LIBOR-OIS spread has widened considerably.

The Fed appears to have been running off its balance sheet a bit faster than it telegraphed last year. The balance sheet should be running off at around $15 billion per month in May, ramping to $20 billion per month by October. So, the quarterly rate should be about $45 billion currently, somewhat slower than the $68 billion pace we measure. If the Fed sustains this pace, LIBOR-OIS spreads should widen by another 10bps.

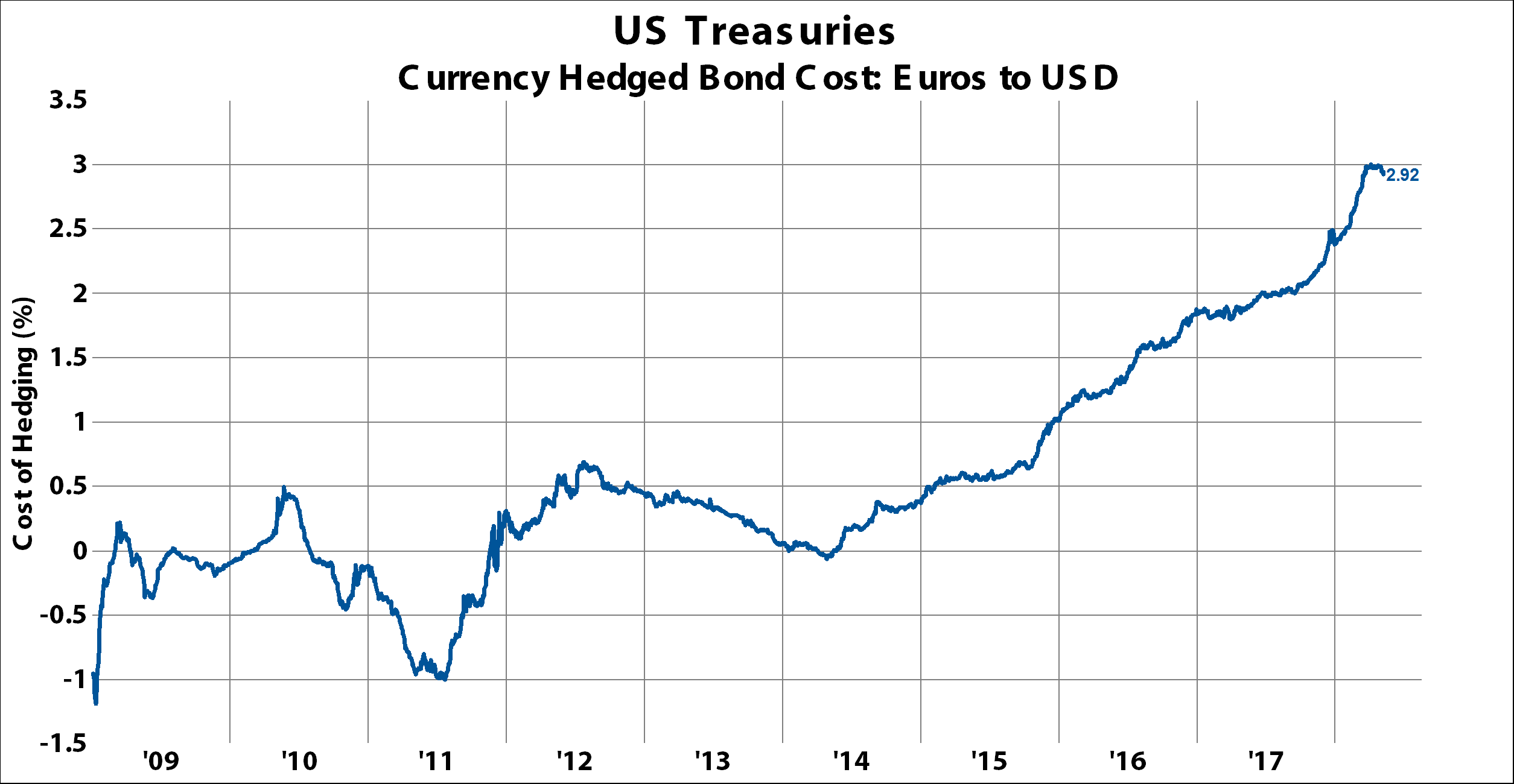

A rising LIBOR rate will add to the cost of hedging the USD. In the chart below, I show the cost of hedging USD/EUR. The principal cost of the currency hedge is the difference in USD LIBOR and EURIBOR. Assuming the ECB doesn’t begin to raise rates until the middle of 2019 and that the Fed continues to raise rates and shrink its balance sheet, the cost of hedging is going higher. Unless US Treasury rates rise, the cost to hedge the USD will be much greater than the yield of the asset to begin with, making them very unattractive for European buyers.