Tale of the Tape: Equity Investors More Concerned About Rising Inflation Than Slowing Growth

July 23, 2018We calculate statistics for all developed and emerging equity markets around the world. For our mid/large cap indexes, we take the top 85% of all stocks in a given region or country and convert all prices into US Dollars. These Knowledge Leaders Selection Universe (KLSU) Indexes form the basis of our investment products. By calculating our own statistics, we gain a more intimate relationship with the granular detail of global equity markets.

There are some major technical divergences occurring underneath the surface of the developed world equity markets. These divergences relate to the performance of the largest companies vs. the performance of the average company. We calculate market-cap weighted price indexes to see the market through the lens of standard benchmarks like the S&P 500 or MSCI World Index. We also calculate equal-weight price indexes, where the impact of every stock is equal. Sometimes, these series diverge, offering some insights into sector leadership trends. In general, we find that equal-weight indexes provide better insight into opportunities for portfolio alpha since they reflect more accurately how the majority of stocks are performing. We prefer to invest in areas where the majority of stocks are outperforming so our chances of selecting an outperforming stock is higher (i.e., the “hit rate”). There are several divergences to note that contain information content about asset allocation.

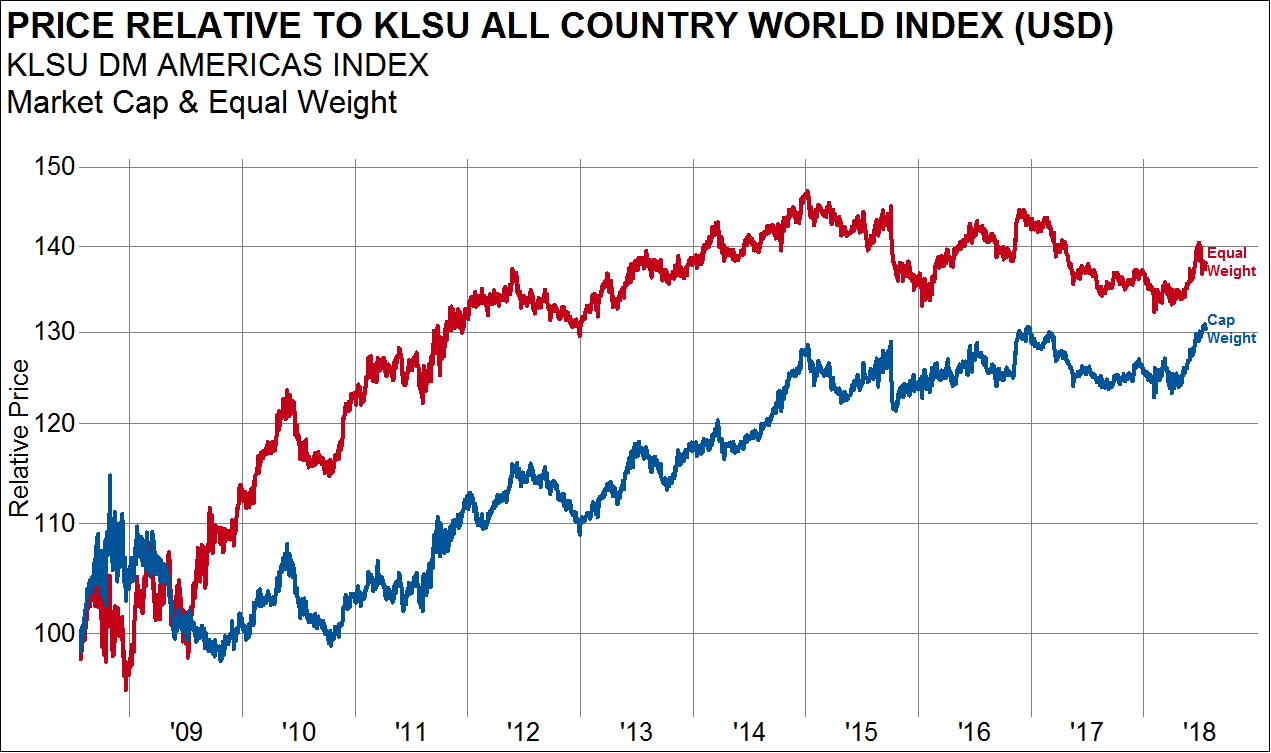

Our KLSU America market-cap weight index is breaking out to new highs relative to our KLSU All Country World Index. But, our KLSU Americas equal-weight index peaked at the end of 2014 and has been making lower highs and lower lows for three years now. While the average stock peaked years ago and is struggling recently, the largest companies continue to see share prices rise. This is a pretty good signal that relative leadership is shifting away from the US.

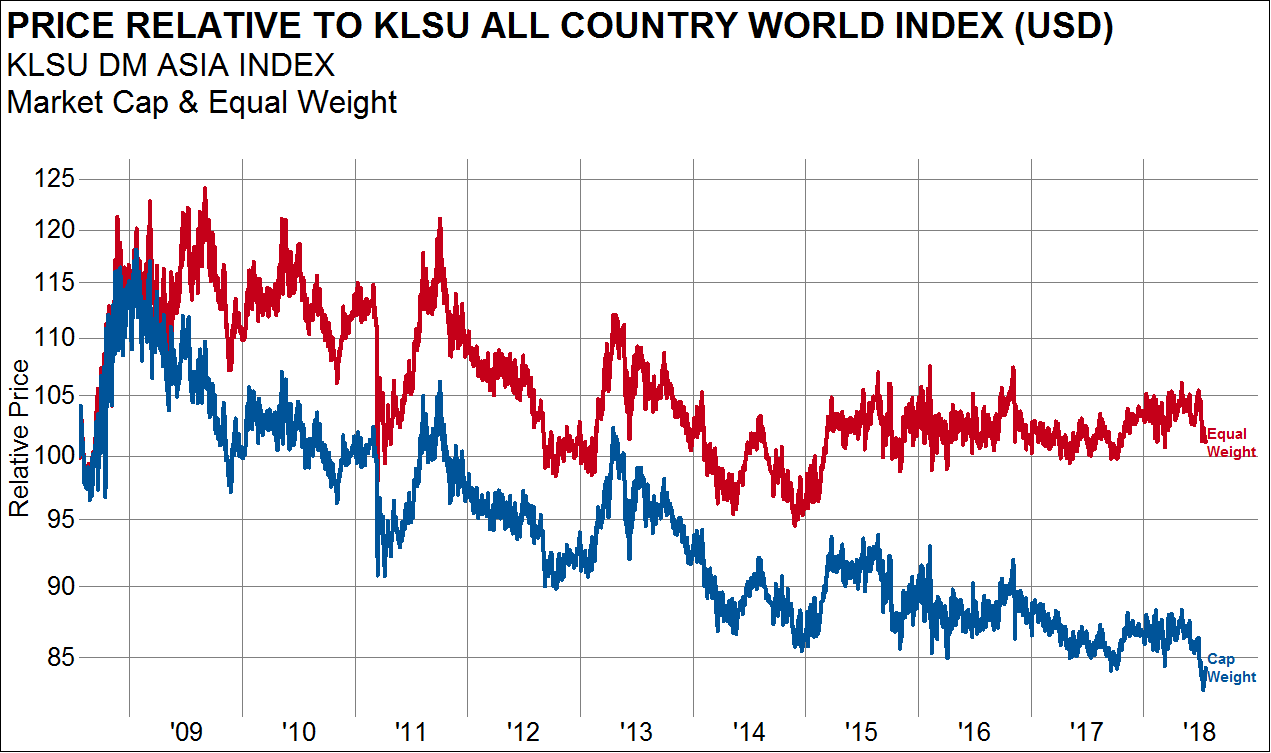

On the other hand, our KLSU Asia Index market-cap weight is making new decade lows while our equal-weight index has outperformed global equities by about 5% since the end of 2014. This is the opposite situation as above, where the average stock has been doing well while the largest companies struggle. This is a pretty good sign that relative leadership is shifting to developed Asia (Japan, Australia, Singapore, New Zealand).

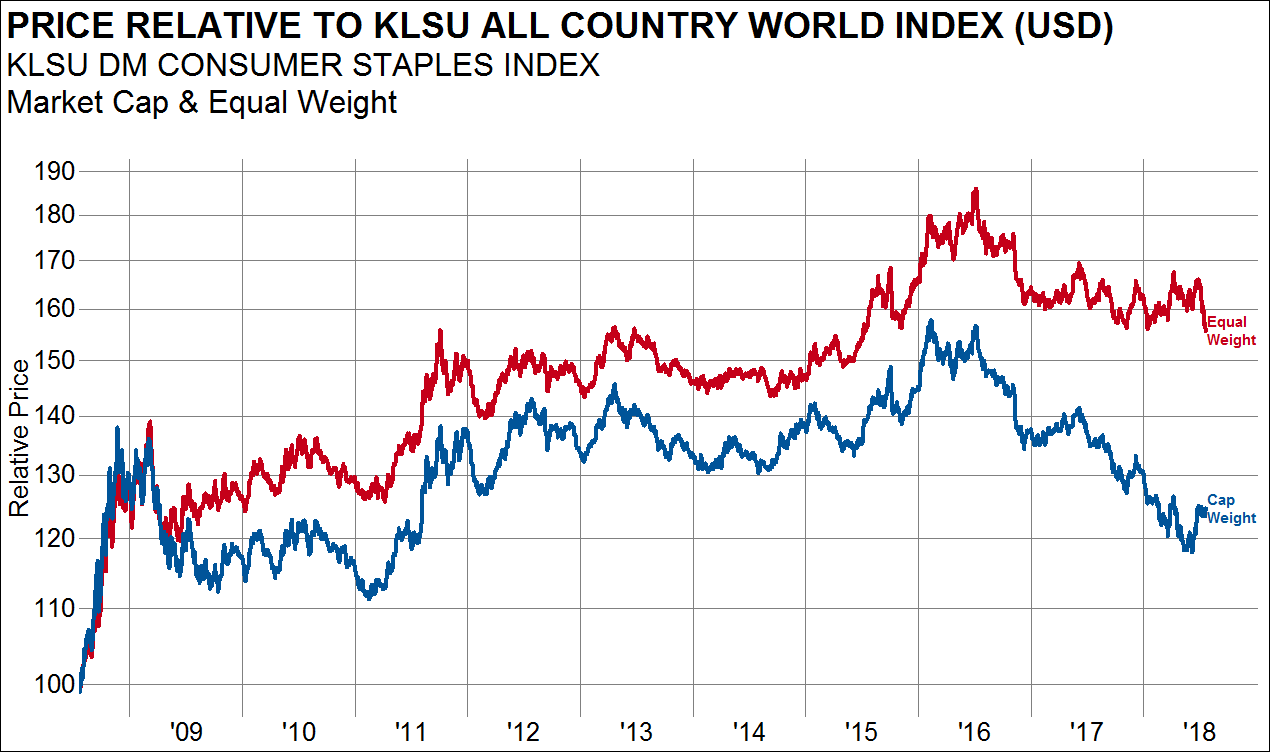

On the surface it would appear that the defensive consumer staples sector has outperformed recently as investors worry about global growth. But our equal weight KLSU Developed Market Consumer Staples Index is making new lows. Global consumer staples are not sending a signal of defensive positioning. I think this reveals that contrary to headlines, investors are more concerned about inflation than growth. As long as this continues, consumer staples are a portfolio underweight.

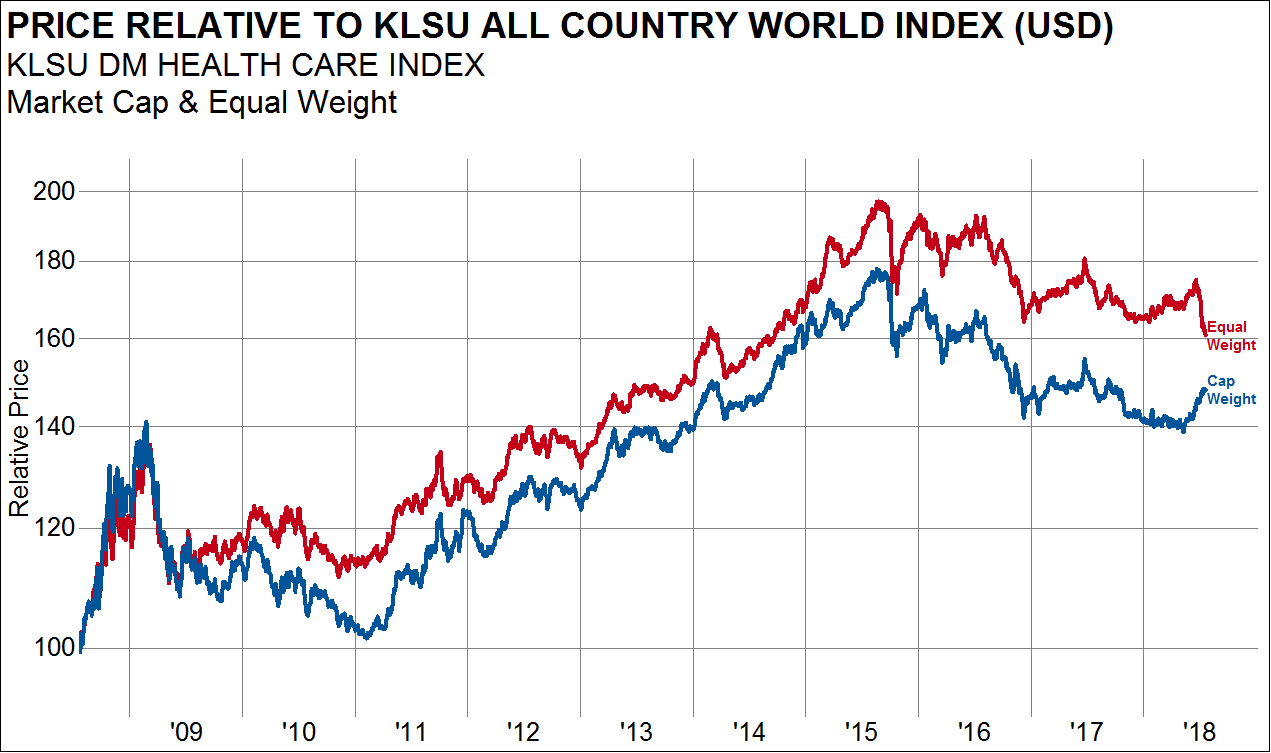

We see the same divergence happening in another traditionally defensive sector, health care. Our equal-weight KLSU DM Health Care Index is breaking to new lows while the market-cap weight index appears to bouncing. So, while a few large health care companies are doing well, investors are moving out health care en masse.

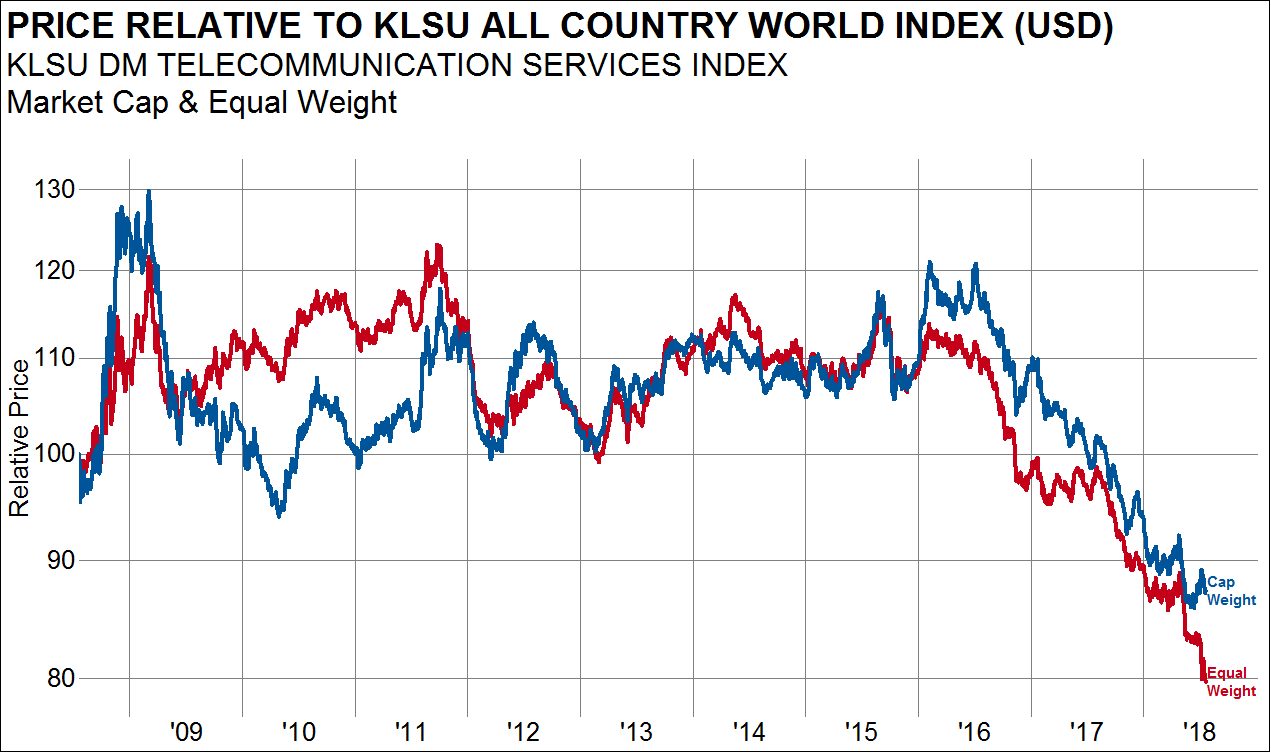

The telecommunications sector is exhibiting a similar divergence. The equal-weight KLSU DM Telecommunications Index is making new decade lows, accelerating on the downside. Clearly, this is an area of liquidation.

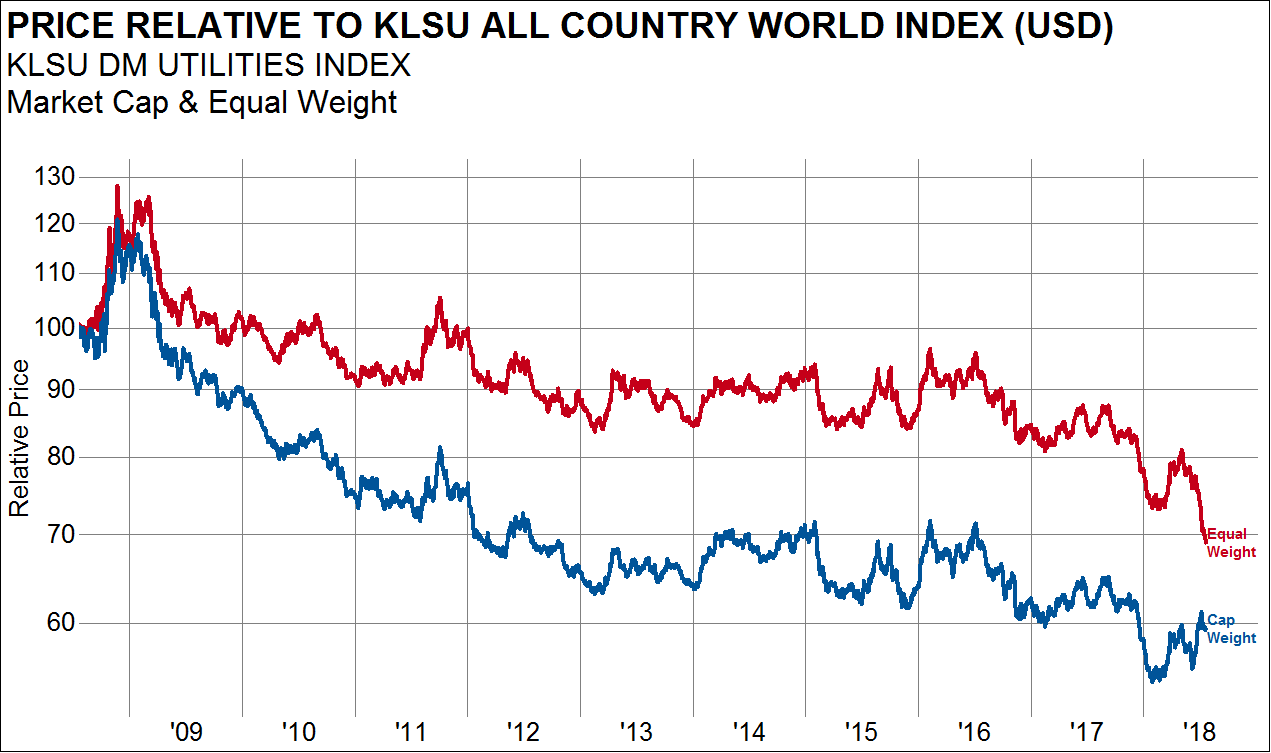

And, touching on the last defensive equity sector, our equal-weight KLSU DM Utilities Index is making new lows as well. While the largest stocks have held the market-cap weight index up, the average stock is performing poorly.

To summarize what we have seen so far: all four of the traditionally defensive sectors are exhibiting negative divergences where the average company is either making at least new two-year lows (staples) or new decade lows (telecom and utilities). This is pretty strong evidence that there has been no defensive turn in equity positioning. Quite the contrary, all counter-cyclical sectors are undergoing liquidation, suggesting investors are more concerned about rising inflation than faltering growth.

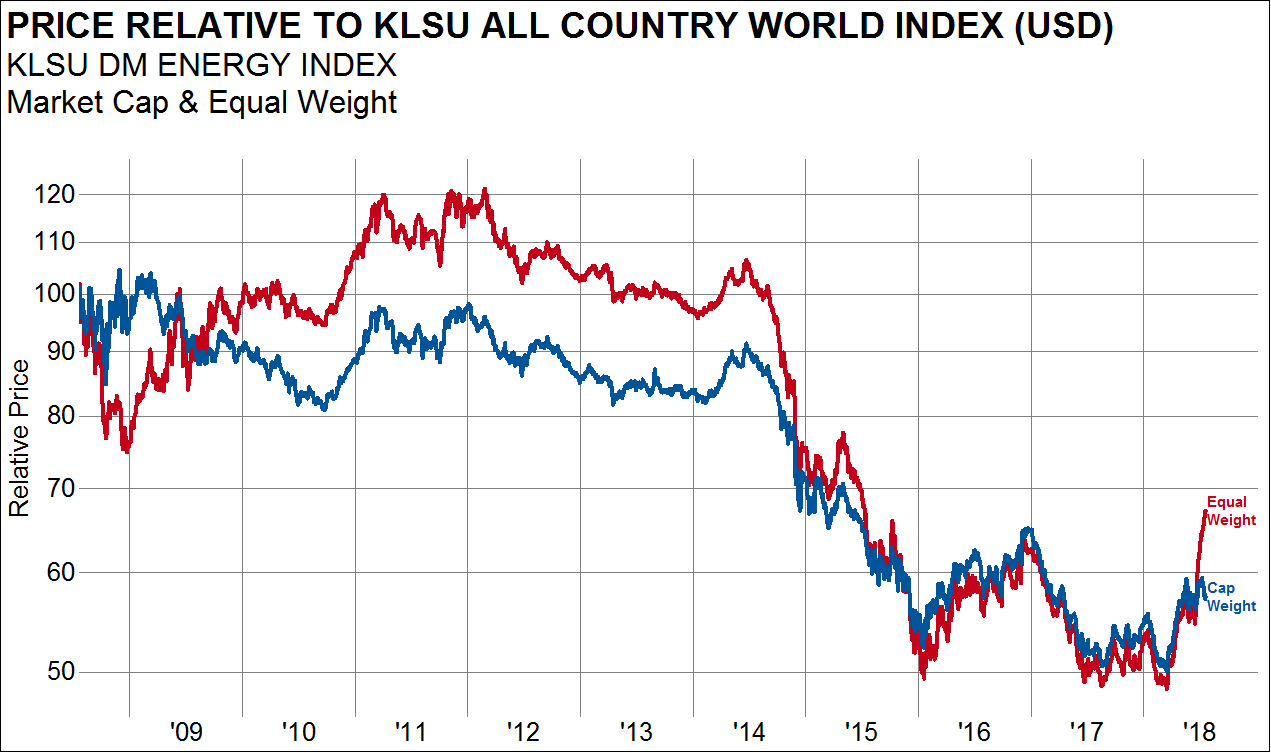

This exodus from defensive stocks is occurring while our equal-weight KLSU Energy Index is surging, moving well ahead of the market-cap weight index. This suggests that investors are indiscriminately buying global energy companies.

The relative performance of our equal-weight KLSU DM Energy Index is highly correlated to oil prices, more highly correlated than the market-cap weight index. Energy stocks have re-synced with the move higher in oil prices.

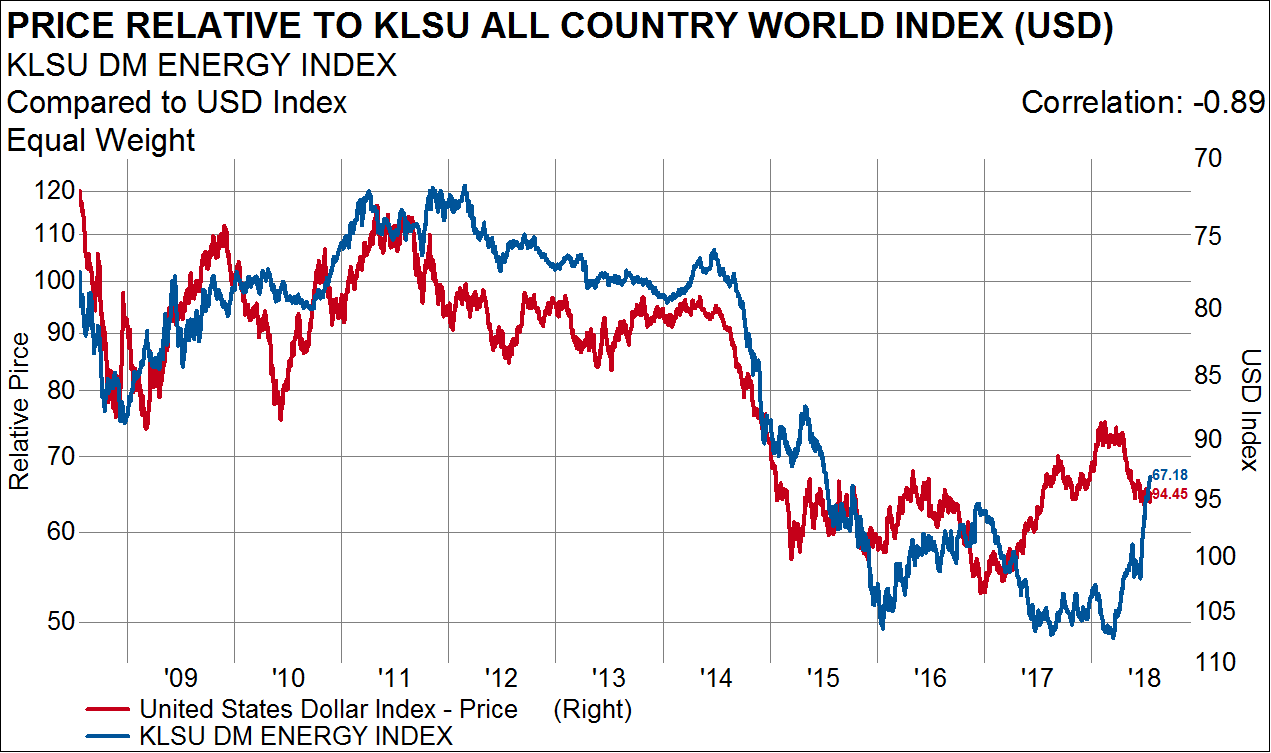

The relative performance of global energy stocks is even more highly correlated with the US Dollar, at 89%.

Perhaps this is the most important signal that investors are more concerned about inflation than growth. Investors seem to be seeing through the counter-trend move in the USD Index, positioning for a lower USD and resulting higher growth and inflation.